English

English русский

русский Français

Français Español

Español Deutsch

DeutschIndustrial valve industry layout

We specialize in the design and manufacture of high quality valves and are committed to providing our customers with excellent fluid control system solutions.

Against the backdrop of an average industrial added value growth rate of 2.53% and a manufacturing added value growth rate of 2.69%, the global output of industrial valve products reached 19.4 billion pieces in 2019, with the proportion of industry and papermaking increasing most significantly, and the demand in the oil and gas sector accounting for a relatively low proportion. The following is an analysis of the industrial layout of the industrial valve industry.

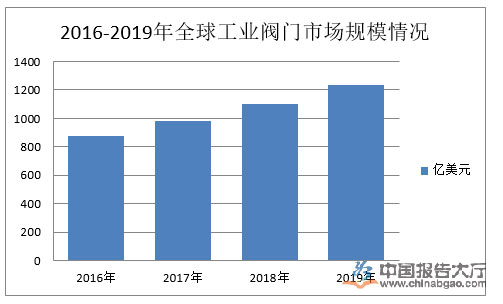

The sustained and stable growth of the global economy has driven the development of downstream industrial valve industries, including oil and gas, power generation, water treatment, chemicals, and urban construction. Industrial valve industry analysis indicates that the global industrial valve industry is rapidly developing, and the industrial valve industry has also achieved rapid growth. In 2019, the global industrial valve market size reached US$123.56 billion.

Industrial valve industry landscape analysis indicates that in 2019, my country's industrial valve market size reached US$12 billion, accounting for 19.5% of the global market. Based on the development speed and investment intensity of various domestic industries, the proportion of the domestic industrial valve market in the global market is steadily increasing. In 2020, the global industrial valve market size will be approximately US$64 billion, with my country's share expected to reach 20%-21%. This translates to a domestic market size of approximately US$12.8-13.5 billion in 2020.

From a market perspective, domestic valve companies are mostly located in the low-end of the valve industry. Valves in this low-end market are highly versatile, have low technical requirements, and have low barriers to entry. The industry is highly competitive with a large number of companies, resulting in low market concentration. With the increasing number of new entrants in the industry, competition will intensify, and profit margins in the low-end valve market will decline.

From a business perspective, the domestic valve industry is undergoing an accelerated reshuffle, with large valve manufacturers likely to emerge as prominent players in the future. On the one hand, small and micro-sized enterprises with less standardized operations and weaker core competitiveness are gradually exiting the market, while the market share of large domestic valve companies is steadily increasing. On the other hand, domestic valve companies still have considerable room to grow in size compared to international giants (only Newway has revenue exceeding 2 billion yuan, while approximately 7-8 companies have revenues between 1 billion and 2 billion yuan). I believe that with the recovery of the downstream market and the improvement of companies' international competitiveness, the market share of leading domestic companies, represented by Newway, will continue to increase in 2020, potentially creating a global leader in mid-to-high-end industrial valves.

Currently, my country's industrial valve manufacturers are primarily concentrated in Zhejiang, Jiangsu, and Shanghai. There are 26 valve companies listed on the Shenzhen, Shanghai, Hong Kong, and National Equities Exchange and Quotations (NEEQ) markets. The industrial valve industry landscape indicates that these 26 valve companies range in size and product offerings, providing a true reflection of the current state of domestic valve companies. In 2019, 17 of the 26 companies mentioned above achieved revenue exceeding 100 million yuan, with Newway Group leading the industry in both revenue and net profit.

my country is now capable of producing over 3,000 models and 40,000 specifications of industrial valve products. These include gate valves, globe valves, throttle valves, plug valves, ball valves, butterfly valves, diaphragm valves, check valves, safety valves, pressure reducing valves, steam traps, and regulating valves, totaling twelve categories. Petrochemical and coal chemical valves, as well as valves for long-distance pipelines, are key areas for new product development in the industrial valve industry during the 13th Five-Year Plan.

Overall, my country's industrial valve companies remain relatively small compared to their foreign counterparts, resulting in a relatively fragmented market. my country's industrial valve industry exhibits overcapacity in the low-end industrial valve market, strong competition in the mid-range industrial valve market, and a monopoly by foreign companies in the high-end and specialty industrial valve markets. It is expected that the improved prosperity of downstream industries will drive an increase in related fixed asset investment, thereby driving demand for industrial valves. This concludes our analysis of the industrial valve industry's landscape.

Your email address will not be published. Required fields are marked *

Contact Information

ADD: No. 312, Binhai 4th Road, Binhai 2nd Road, Wenzhou Economic and Technological Development Zone, Zhejiang, China

FAX: +86-577-86901099

PHONE: +86-18267823456

TEL: +86-577-86070000

E-MAIL: [email protected](FT Dept. I)

[email protected](FT Dept. II)

[email protected](FT Dept. III)

[email protected](FT Dept. IV)

Copyright © Zhejiang Dico Valve Co., Ltd. All Rights Reserved. 浙ICP备2020033083号

Flanged Ball Valve Supplier